Mohnish Pabrai’s Coal Bet

How to Copy Investors the Right Way—and Why I Invested €30,000 in Two Coal Companies I Know Nothing About

Mohnish Pabrai is one of the investors I mentioned in Investing Principle #4—an investor whose biggest bets I’m willing to follow blindly with a small part of my portfolio. And that’s exactly what I did here. Let me explain…

Summary

A while back, I listened to Pabrai’s lecture at the University of Nebraska, where he mentioned looking into the coal industry. By the end of 2024, he went all in—putting 100% of his $200 million partnership into three coal companies. This is a bet on metallurgical coal, essential for steelmaking—not the energy-producing thermal coal.

He also runs a mutual fund with at least 15% allocated to the same coal stocks.

I put 10% of my portfolio into this bet because I know Pabrai has done the work—and has real skin in the game. I have no interest in digging deep into the U.S. coal industry and I don’t see myself reaching a different conclusion anyways.

So, on February 3rd, I bought

131 shares of Alpha Metallurgical Resources at $180.50

130 shares of Core Natural Resources at €88.07

Both stocks have dropped significantly since then, and I’m thinking about adding to my position.

Why Does Pabrai Believe in Coal?

To understand his bet, I recommend watching the first 20 minutes of this interview.

Here are my key takeaways:

The coal industry is highly cyclical, experiencing repeated boom-and-bust cycles driven by coal prices.

During boom periods, many coal companies take on significant debt to expand.

When prices fall, some companies struggle to service their debt and go bankrupt.

This reduces supply, which pushes prices back up, restarting the cycle.

Pabrai identified three coal companies that took a different approach during the recent boom:

They avoided excessive debt, instead paying it off completely and even buying back shares.

They are low-cost producers, able to break even in the current downturn.

With no debt and breakeven operations, they are positioned to survive the bust cycle and generate massive profits when coal prices rebound.

Coal prices might stay low for a long time. But that scenario is already priced in, which is why these stocks trade at such low valuations.

That’s all there is to it. I didn’t look any deeper.

But the real question is: Why do I trust Pabrai almost blindly?

Why Do I Trust Mohnish Pabrai?

Pabrai has spent decades proving his ability to spot asymmetric bets. His story is remarkable. Born in India, he saw firsthand how his father pursued various entrepreneurial ventures—some successful, most not.

He moved to the U.S. to study and later built an IT consulting business that grew to $20 million in revenue. Along the way, he discovered Buffett’s annual letters and became obsessed with value investing. After selling part of his company for $1 million, he shifted his focus to investing full-time. Within five years, he turned that $1 million into $13 million and started managing money for friends and family. Today, he oversees about $1 billion.

Pabrai achieved his returns by sticking closely to Buffett’s value investing principles, even copying some of his trades. He gained broader recognition in 2007 when he paid $650,100 in a charity auction to have lunch with Buffett. After the lunch, Buffett introduced him to Charlie Munger, and they remained close friends until Munger’s passing.

He also wrote The Dhandho Investor, which I consider one of the best investing books ever written. While his principles are rooted in Buffett’s teachings, he presents them in a different context, making them highly accessible.

Dhandho is a Gujarati term meaning "endeavors that create wealth." The book explains low-risk, high-reward bets through examples of successful Indian entrepreneurs, such as the Patel family, who built vast motel businesses in the U.S. with minimal capital. Two core ideas from the book have stuck with me:

"Heads I Win, Tails I Don’t Lose Much"

Pabrai looks for asymmetric risk-reward opportunities—situations where the downside is minimal, but the upside is large. His ideal bet is "risk $1 to make $10."The Kelly Formula

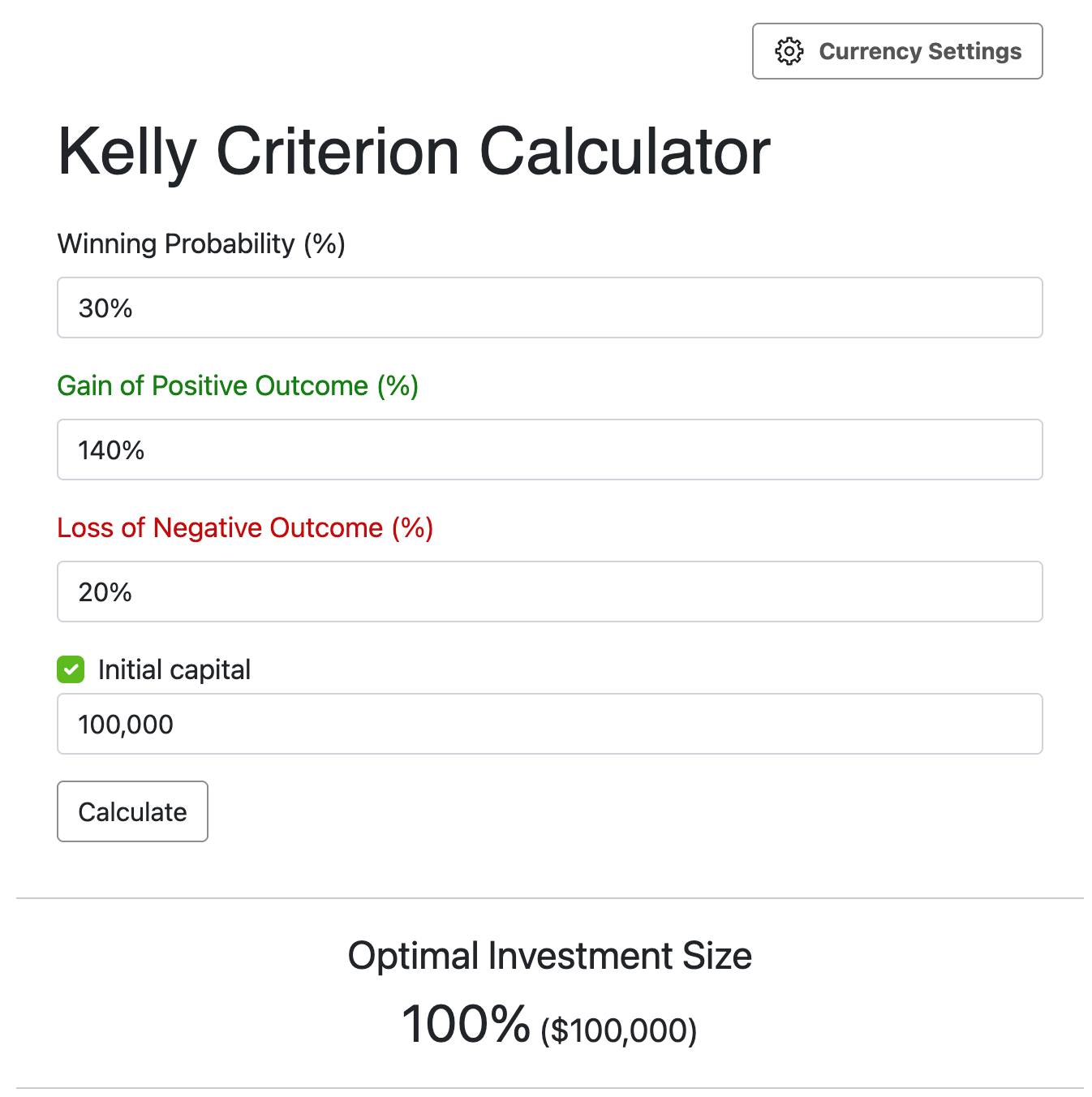

If you find such an opportunity, bet big. The Kelly Formula helps determine the optimal percentage of capital to allocate based on estimated probabilities and returns.Example: If the probability of success is 30%, the expected gain is 100%, and the potential loss is 20%, the Kelly Formula suggests betting 80% of available capital (see calculation).

Understanding these principles helps me make sense of Pabrai’s all-in move on coal. I didn’t follow his investment because I’m convinced he’s right—I followed it because I’m convinced he believes he found an asymmetric bet.

Maybe he estimates his winning probability at just 30%, fully expecting to lose such a bet most of the time. But if the expected loss is low (say, 20%) and the expected gain exceeds 140%, the Kelly Formula justifies investing 100% of available capital.

That’s why I have no issue putting 10% of my portfolio into the same bet.

How To Copy Investors the Right Way

Did I just make value investing sound easy? It isn’t.

Keep reading with a 7-day free trial

Subscribe to Till's Value Portfolio to keep reading this post and get 7 days of free access to the full post archives.